Innovation

For the first time, a concrete set of priority actions for the global plastic packaging value chain to trigger an accelerated transition towards the New Plastics Economy has been identified. These actions are based on three major new insights. These insights were revealed through thorough analytical work, including a granular segment-by-segment analysis of the plastic packaging market, numerous interactions with players across the plastics value chain and discussions with over 75 experts. The three insights, which have the potential to drive a genuine transformationwithin the plastic packaging sector and herald the shift to the New Plastics

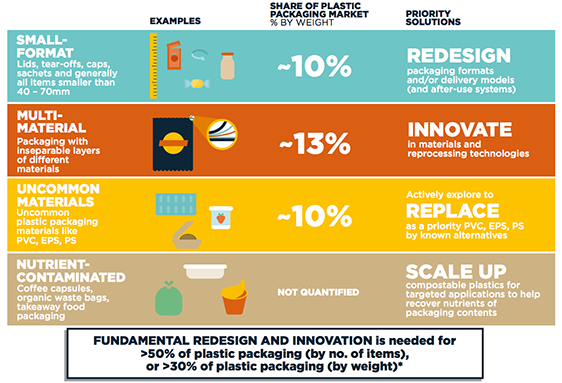

Without FundamentalRedesign and Innovation,about 30% of PlasticPackaging Will Never BeReused or RecycledThis category, representing at least half ofthe plastic packaging items and about 30%of the total market by weight, consists of four segments: small-format packaging; multi-material packaging; uncommonplastic packaging materials; and nutrientcontaminated packaging (see Figure 3).

While often offering high functionality, these packaging types do not have a viable reuse or recycling pathway and are unlikely to have one at scale in the foreseeable future. To shift these segments to a more positive material cycle, fundamental redesign and innovation of materials, formats, delivery models and after-use systems is required.

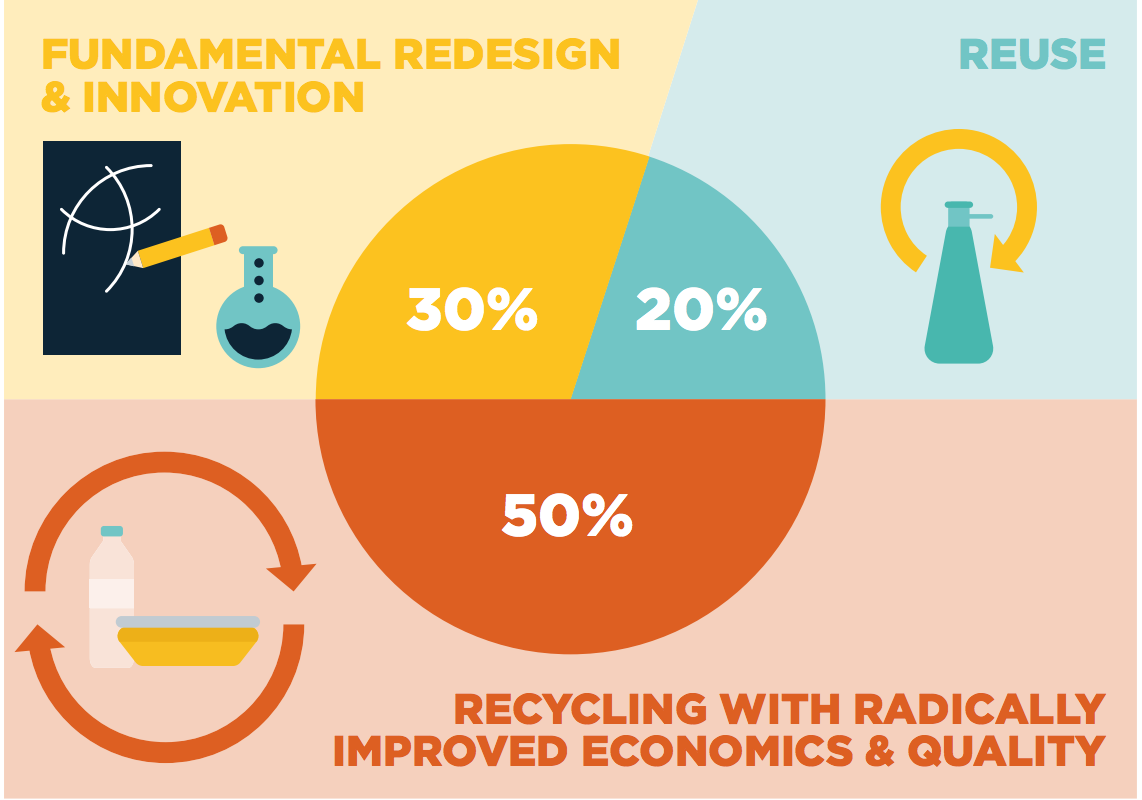

- 1.Without fundamental redesign and innovation, about 30% of plastic packaging will never be reused or recycled

- 2.For at least 20% of plastic packaging, reuse provides an economically attractive opportunity

- 3.With concerted efforts on design and after-use systems, recycling would be economically attractive for the remaining 50% of plastic packaging

after-use value makes them less likely to be collected by the informal sector (i.e.waste management activities carried out bywaste pickers)11 and in advanced economies, where items like lids, caps, straws and sweet wrappers are consistently mentioned as some of the plastic packaging items most found in litter.12 Cleaning up these smallformat items after they have escaped collection systems is particularly hard precisely because they are small. Sachets are a typical small-format example: they are used all over the world, but particularly in emerging markets, to sell products such as condiments and shampoo in small quantities, making them more convenient and affordable. Especially in countries without a formal collection system, many of these sachets end up as litter.

Even when they are collected, small-format items are hardly ever recycled due to significant technical and economic barriers. A study ordered by the industry association, PlasticsEurope, estimated the effective recycling potential for this segment to be zero, even in an optimistic scenario.13 The main barrier is the difficulty of sorting small-format items – a critical step in the recycling process. One of the first stages in automated sorting facilities is a screen that removes all small items, such as loose dirt, stones and other materials that could damage equipment in subsequent sorting steps. During this process, all items smaller than 40mm-70mm fall through the mesh in the screen, end up in the fines fraction, and are sent for energy recovery, incineration or landfill.14 Due to the small size and low value of these items, a successive layer of sorting technology to extract the plastics from the fines fraction is not economically viable and is unlikely to be so in the foreseeable future.15 In theory, manual sorting could perhaps overcome the technical barriers small-format items pose to automated sorting, but it is economically challenging given the low volume-to-time ratio of sorting these items.